You’re not alone if you find it difficult to wrap your head around the Swedish pension system. I’ve been there, and I’ve probably over Googled it too. After all, a good chunk of the taxes you pay go into your pensions, so it’s definitely worth understanding what you’re getting. Who knows, maybe future me will come back here to double-check, too.

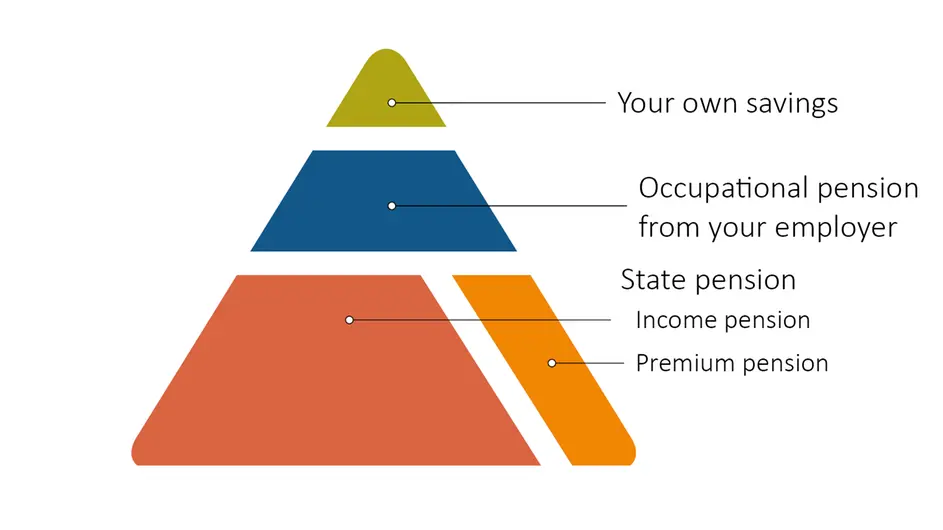

The best way to visualise the pension system is through a pyramid, where various components form the building blocks. It can be broken down into three distinct blocks:

- Income and premium pension

- Occupational pension

- Personal savings

I guess you’ve already gathered what ‘Personal Savings’ implies. So, in this post, I’m going to focus on the first two blocks.

The good news? For most people, these first two blocks will replace 60–70% of your salary when you retire.

The bad news? You’ll need to have the rest saved up. My post about different investment accounts in Sweden could come in handy.

Income and Premium Pension

This block of your pension is part of the public pension scheme. How much you earn is proportional to your income. Each year, 18.5% of your annual income is allocated to your pension, but only up to a certain ceiling, which is recalculated each year (604,500 SEK for 2025). Ceilings are based on inkomstbasbelopp (income base amount).

The inkomstbasbelopp is like Sweden’s official “salary tape measure.”

It stretches a bit each year as average wages grow, so the pension rules keep up with what people actually earn, not just what coffee costs.

This block is further divided into two [18.5% = 16% + 2.5%):

Income Pension

- 16% of your annual income is placed here.

- It’s a fictitious account, which is based on income development in Sweden. Your current contributions are paying for those in pension now.

- When you retire, your pension will be paid by those currently working (Pyramid scheme vibes anyone?).

Premium Pension

- 2.5% of your annual income is placed in an account where you choose how it’s invested.

- You choose up to 5 funds to place your money. If you don’t make an active choice, it’s by default in AP7 Såfa, which historically has had the best returns and the lowest fees (a great default for most people).

- Make your fund choices here.

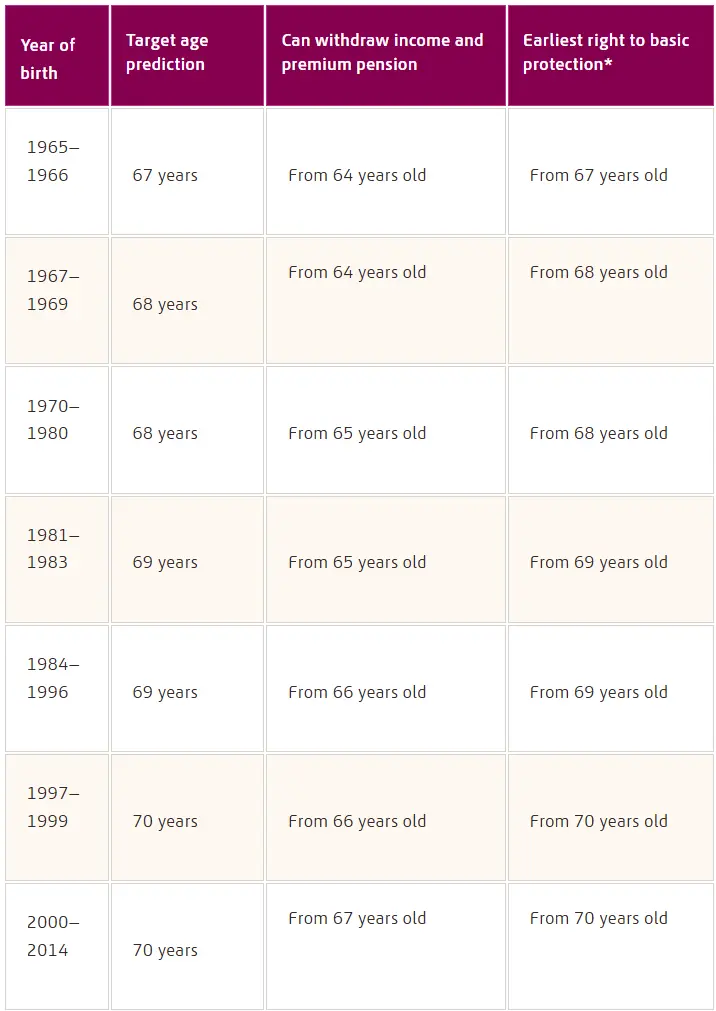

You can start withdrawing from this pot 3 years before your “target retirement age.” And no, retirement age isn’t fixed in Sweden. It depends on how life expectancy develops. Check out the table below to see where things are heading.

It’s daunting to see your retirement age as “70”. But hey, the good news is that this pension is paid out for life, and you can receive it even if you move abroad. So go ahead and dream about that little town in Greece. 🌞

If you haven’t earned much (or at all), you may be eligible for a guaranteed pension, a safety net from the state.

- You’ll need to have lived in Sweden for at least 40 years between the ages of 16 and 64 to get the full amount.

- If you’ve lived here less time, the benefit is reduced proportionally.

It’s only paid once you reach your target retirement age and only if you’re living in Sweden.

Occupational Pension

So, how is an occupational pension different? Contributions are made by your employer. Good to know: By law, employers are not required to make contributions to an occupational pension. However, the vast majority of employers in Sweden have a collective agreement. Therefore, they also have an occupational pension. There are different kinds of occupational pensions depending on the sector you work in (private, state, municipal, etc.). For white-collar private industry, the occupational pension agreement is known as ITP.

There are two types:

- ITP1 (Defined Contribution) – for most people

- ITP2 (Defined Benefit) – for some folks in older agreements

We’ll stick with ITP1, since that’s what the majority of people have.

So, here’s how it works:

Your employer pays 4.5% of your monthly gross salary up to 50,375 SEK, and 30% for anything above that, up to 201,500 SEK (all 2025 numbers).

Why those numbers? The limits are 4.5% up to 7.5 income base amounts and 30% over that up to 30 income base amounts.

Why the extra generosity after the limit? Because employers don’t pay social security tax on salaries above 7.5 income base amounts. So they can afford to be more generous.

What do you need to decide? There are three choices you’ll need to make about your occupational pension:

1. How to invest?

Traditional insurance: Guarantees a payout when you retire, but the insurance company chooses how your money is invested.

Unit-linked insurance: No guarantees, but you pick the funds, which gives you the chance for higher returns (and higher risks).

You must have at least 50% in traditional insurance.

2. Which insurance firm?

There’s a list of approved providers (updated every 5 years via a national tender).

If you do nothing, all your money goes into Alecta’s traditional insurance.

If you want to be proactive, you can split your contributions between providers and choose your funds. The KISS method (Keep It Stupid Simple) is great here: go with broad market and low-fee funds.

3. Do you want a repayment cover and/or family cover?

Repayment cover: Your pension is passed on to your family if you pass away before your ITP1 runs out. But your monthly payout will be lower when you retire. If you don’t have repayment cover, your leftover pension goes into a pool for others in your age group. Morbid, but efficient.

Family cover: An optional add-on that acts like a life insurance policy if you die before retirement. Your family receives a sum: You get to choose how much and for how long. Since nothing is free, costs are extra and reduce your payout.

Other good-to-knows:

- You can start withdrawing from your occupational pension as early as age 55.

- Payouts don’t last for life. They last until the money runs out.

- Payments are paid out over a period you choose (minimum 5 years)

You can receive it even if you live abroad.

Final Thoughts

- You can draw your pensions even if you leave Sweden, except the guaranteed one.

- There’s a great calculator at MinPension.se if you want to see how your pieces stack up.

I’m working on my own calculator too, one that tells you how much extra you might want to save to retire comfortably.

Let me know if you made it this far — I’m impressed! Hopefully, this helped you make a little more sense of something that otherwise feels like a bureaucratic escape room. You got this.

And hey, if you want a nudge when the savings calculator is ready, subscribe for updates!