If you have found your way to mykronor, you’re likely somewhat familiar with what you’re going to read. However, I want mykronor to be accessible to everyone, whether you’re a total novice or a seasoned investor. Therefore, I thought it would be good to cover some basics of investing.

Stocks and funds are ubiquitous in the investing community. If you live and work in Sweden, you likely already have some of your money invested in these instruments (hint: it’s your pension). This makes it even more important to have a basic understanding of how they work. So, let’s get into it.

What are Stocks and Funds?

A stock (or share) is a piece of a company. Buying a stock is buying a small piece of a company, it’s as simple as that.

So how small is “small”? For most public companies, a single stock is a teeny tiny fraction. Let’s take Netflix (NFLX) as an example. One share of Netflix is currently valued at ~10,800 SEK, a significant sum for most people. However, this only represents 0.000000235% of the company.

A fund, on the other hand, is a collection of shares. When you buy into a fund, you’re spreading your money over many different companies. A simple analogy: buying a Netflix stock is like buying a single banana, but buying a fund is purchasing the whole fruit basket. So you don’t just get a banana, you also get some apples, oranges, pears, and more.

Why Diversify?

A core principle of sound investing is diversification. Going back to baskets, it’s about not having all your eggs in one basket.

Imagine putting all your money into Netflix. You would be tying your financial future to how Netflix as a company performs. While it has done incredibly well so far, are you sure it will continue to do so for the next 40–50 years? History suggests the odds are low.

This is where funds, especially index funds, come in. They offer the benefit of instant diversification. Your savings would be spread over hundreds of companies, including Netflix today and Netlfixes of the future.

Index Funds vs Actively Managed Funds

An index is simply a list of companies, like the S&P 500 (America’s 500 largest companies) or OMXS30 (Sweden’s 30 largest companies). They spread your money across the biggest companies in the market.

Which index should you choose? That depends. You could select an index that follows the global stock market, the European stock market, the US, or any other country. The key is that you’re investing in an automated, low-cost strategy that has historically been highly successful. It’s quite simple in that as long as the global economy grows over the long term, your money can grow too.

An actively managed fund, however, is one where someone selects which stocks to include. You pay someone to manage your money, usually a percentage of your investment. Index funds also have fees, but the key difference is how much you pay.

Why Do Fees Matter?

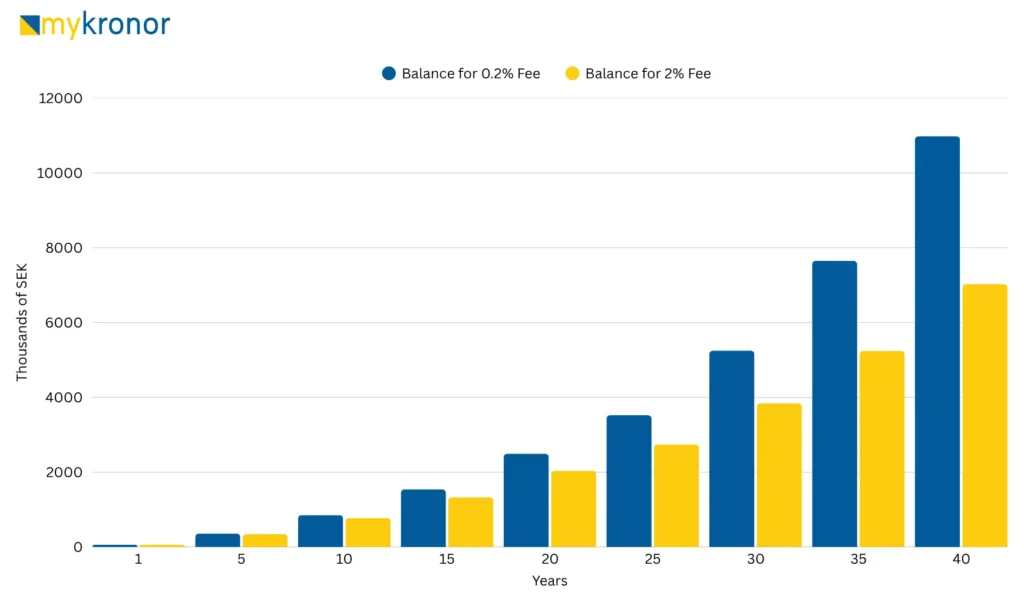

Most actively managed funds charge around 2%, while index funds range from 0–0.2%. I know that 2% doesn’t sound like much, but here’s the kicker: a 2% fee compounded over 40 years will end up costing you around 35% of your total returns!

Let’s put these numbers into perspective. Imagine investing 5,000 SEK per month for 40 years at a 7% annual return:

| Initial Investment (SEK) | Monthly Contributions (SEK) | Fee (%) | Total Fees Paid (SEK) | Investment Value After 40 Years (SEK) |

|---|---|---|---|---|

| 0 | 5,000 | 0.2 | 572,880 | 10,983,504 |

| 0 | 5,000 | 2 | 4,526,660 | 7,029,724 |

That’s a difference of ~4 million SEK, enough to buy a house in many Swedish cities!

Most fund managers claim they can beat the market, i.e. exceed the 7–8% annual growth that indices typically provide, justifying higher fees. Is there any truth to that? A recent report shows that only 5-10% of actively managed funds beat the market over a 20-year period. That means the likelihood of losing money by trusting a manager is 90-95%. I think those numbers speak for themselves.

If you would like to play around with your own numbers, here’s the tool that I used.

Historical Returns

I thought it would be a fun exercise to highlight further how tricky stock picking can be, using some comparisons.

I’m going to compare the performance of two stocks: Amazon and Citibank, with the S&P 500 index, which consists of the 500 most valuable companies in the US. The table below summarises how much 1,000 SEK invested into each in 1998 would turn out to be today.

| Investment | Initial Investment in 1998 (SEK) | Total Investment Value in 2025 (SEK) | Annual Compounding Rate (%) |

|---|---|---|---|

| Amazon | 1,000 | 94,708 | 18.4 |

| Citi Group | 1,000 | 1,950 | 2.5 |

| S&P 500 | 1,000 | 6,269 | 7 |

If you had picked Amazon in 1998, you would be wealthy. However, there are far more companies like Citi than Amazon, so finding a stock with Amazon-like returns is like finding a needle in a haystack. On the other hand, if you had picked the S&P 500, which includes both Amazon and Citi, you would still end up with an annual return of 7%.

7% isn’t bad at all. In the example above, if you had invested 1,000 SEK every month since 1998, you would have accumulated 900,000 SEK, of which 575,000 SEK would be gains! Being consistent and disciplined is the key to building long-term wealth.

Avoid the Pitfalls

Investing is a marathon, not a sprint. The most common mistake new investors make is succumbing to fear.

Markets swing in the short term, but long-term trends generally move upwards. Observe the world index below. Can you spot the COVID-related drawdown?

It represents a 20% drop. Selling during such times would have made you miss the 130% gain that followed. Patience is crucial.

Final Thoughts

- Start early and stay consistent – small, regular investments grow substantially over time.

- Diversify your investments – it protects you from market fluctuations.

- Be mindful of fees – lower fees greatly impact long-term returns.

- Avoid chasing individual stocks – index funds are reliable, low-cost, and powerful.

- Stay calm during market swings – short-term drops are normal; long-term growth matters most.

Investing isn’t about being lucky, it’s about being patient.

You might want to check out my post on different investment accounts in Sweden if you’re unsure about how to get started.