I believe this topic could challenge some of our conventional beliefs. For many people, buying rather than renting seems like an obvious choice. Conventional wisdom suggests that buying is always better if you plan to live somewhere for the long term. You’ve probably heard:

“Buying a property is always a good investment.“

“Why would you want to throw money away on rent when you could be spending that on owning your home?“

“You’re helping your landlord pay off his mortgage when you could be paying yours off instead.“

However, I want to challenge these beliefs and look at the data from a wealth-building perspective. While there are numerous websites and simulators for other countries that compare renting vs buying, I couldn’t find one focused on Swedish mortgage laws and tax rules. So, I built my own.

My simulator is a Python script based on Sweden’s housing regulations, including interest rate deductions, amortisation requirements, and capital gains taxes. The math is universal – a compound interest calculator. All it does is look at the difference for your monthly and opportunity costs of renting and owning. It then extrapolates this over a number of years to show what the difference in wealth accumulation would be.

Spoiler alert: Buying a property isn’t always the best financial investment.

Comparing Renting and Buying in Sweden: The Case of Bamse

To illustrate this, let’s use an example based on average housing figures and mortgage rules that come into effect in 2026.

Meet Bamse, a happy bear who lives in Stockholm. Bamse is considering buying a bostadsrätt (a cooperative apartment). The apartment he’s looking at costs 5,046,000 SEK, the average price for a 60 sqm flat in Stockholm. He currently rents an apartment of the same size for 10,000 SEK per month. (That’s slightly above average, but we’ll stay conservative.) Bamse plans to stay for the next 30 years, whether he buys or continues renting. Let’s compare the two paths.

Scenario 1: Buy the Apartment

There are several factors for Bamse to consider when buying an apartment.

Down payment

From 2026 onwards, the minimum down payment will be 10% of the purchase price. For Bamse, that’s 504,600 SEK. Luckily, he has this saved in index funds, ready to sell (I think he follows mykronor).

Interest rate

This is a bit tricky, since interest rates are not fixed in Sweden. Historically, it’s been a better deal to have a mortgage with a floating interest rate. Bamse is going to assume that his interest rate will average around 3% for the next 30 years. Lucky for him, the government allows him to deduct the interest from his taxes. This is 30% up to 100,000 SEK and 21% beyond that each year.

Amortisation

Under Swedish mortgage rules, borrowers must repay part of their loan each year depending on the loan-to-value (LTV) ratio. To get this, you divide the amount you borrow from the bank by your apartment’s value. The table below shows what it would look like for different ratios:

| Loan to Value (LTV) | Amortization (%) |

|---|---|

| LTV > 0.7 | 2% |

| 0.5 < LTV ≤ 0.7 | 1% |

| LTV < 0.5 | 0% |

Since Bamse will start with a down payment of 10%, he is borrowing the other 90%. This means he will have an initial amortisation cost of 2% per year.

Annual maintenance cost

When you own your apartment, you’re also responsible for maintaining it. And eventually something or the other will break. It’s best to set aside a sum every month for that eventuality. You might not need it every year, but when you do, you’ll be thankful you saved. It’s best to save between 0.5% to 1% of your apartment’s value every year.

Bamse thinks the apartment he’s considering buying is in very good condition, so he plans to save 0.5% every year.

Bostadsrätt avgift (Association fee)

This is a fee that you pay to the housing association which owns your building. They use this for maintaining the premises, hiring cleaning services for common areas and making any upgrades to the building or surroundings. This fee can vary significantly depending on the finances of the association.

For Bamse, however, this is 4000 SEK per month if he were to buy the apartment (Also an average!).

Apartment value growth

Apartment values do appreciate over the years. In Sweden, housing prices have historically followed inflation, except in the 2000s and early 2010s when it outperformed its historic rate.

In Stockholm, prices have increased 2.5% every year over the last decade. So Bamse is going to assume a similar rate.

Capital gains tax

If you were to eventually sell your apartment, you would have to pay tax on the profit. In Sweden, this is 22% of the profit. This is also a cost Bamse needs to take into account when extrapolating his wealth.

Scenario 2: Keep Renting

Renting offers simplicity and flexibility, with fewer financial variables.

Monthly rent

Bamse’s current monthly rent is 10,000 SEK for a 60 sqm apartment.

Annual rent increase

Rental prices increase every year or so. Over the last decade, rentals in the Stockholm area have risen around 3% per year. Bamse uses this figure for future projections.

Investments

One of the advantages of renting for Bamse would be to keep his investments in index funds. Along with this, since his monthly expenses will be lower if he continues to rent, he can keep investing his excess savings. Bamse expects a 6.5% annual return, a conservative estimate accounting for ISK taxes.

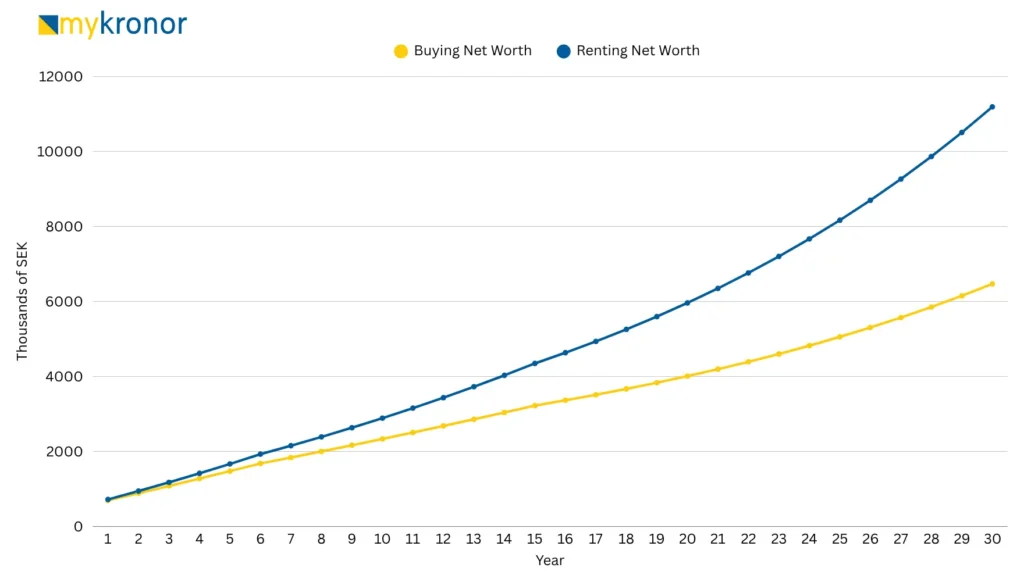

Results

After simulating both paths for 30 years, Bamse’s net worth results are eye-opening:

Buying the apartment – 6,467,966 SEK

Keep renting – 11,187,890 SEK

So Bamse would be ~4.7 million SEK richer if he were to keep renting. Seems counterintuitive, doesn’t it? Well, let’s look at the plots below.

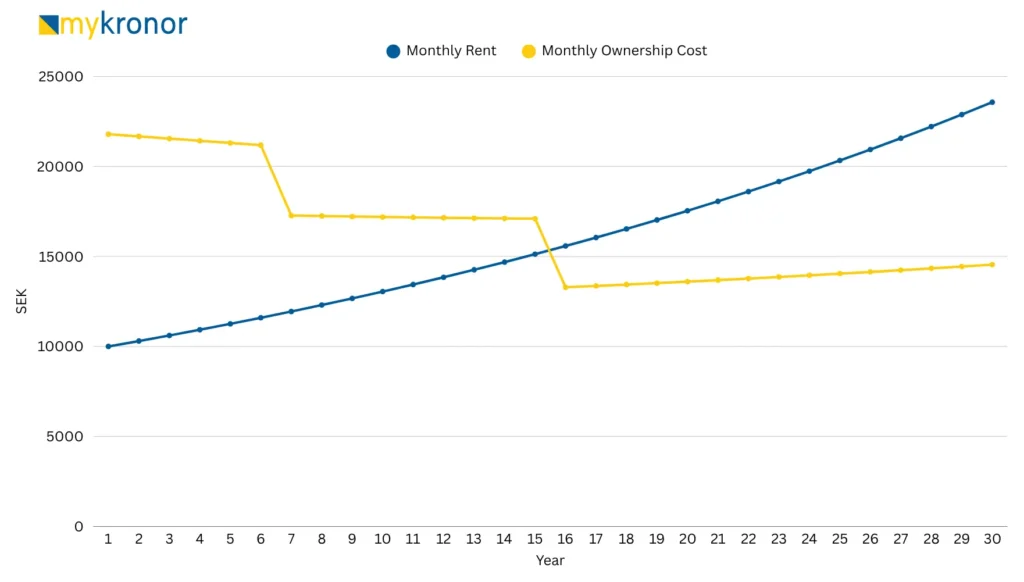

What’s interesting is that by year 16, Bamse’s monthly expenses as a homeowner would be lower than renting. But by that point, his investments from renting would already have grown for 15 years, creating an enormous compounding advantage. This shows the magic of compounding; it’s often about starting early and being consistent. Even though by year 16 Bamse could start investing the savings from owning, it’s too late to catch up.

The story of Bamse is a simple thought exercise. His story mirrors the reality for many people in Sweden. While buying feels like a rite of passage, it’s not always the best financial move. This might seem unique to Sweden, but it’s actually true for most developed countries.

I will not say that housing can never be a good investment. There are markets where you can get much higher returns, even in Sweden. This will require a lot of skill and research to identify, not too different from trying to pick individual stocks.

Predicting the future

To the people who say that future returns on housing will be higher than the past, you might be right. You can never predict something with 100% certainty. Although I would point to the growing frustration in many Western countries, where housing has become an investment vehicle. Even in Sweden, housing is expensive relative to wages because of the boom in housing prices in the 2000s.

What does all that mean? Would the government eventually be persuaded to use policies that make housing affordable? How would that look? It could mean easier permits to build more housing, removal of interest rate deductions (props up housing prices), higher property taxes (disincentivise housing as an investment), etc. All that would mean stagnating or lower housing prices in the future.

Final thoughts

So what’s the point of buying a house? The point is that you’re buying a home. There is psychological safety and emotional stability in knowing that you own your home. It’s where you build memories, raise your family, and create a sense of belonging.

It can also mean buying access. In many attractive neighbourhoods of Stockholm, it’s impossible to find an affordable rental without decades in the housing queue. In these instances, buying an apartment or house is the only choice.

This article isn’t a rant against homeownership. Rather, it’s an invitation to think twice before treating housing purely as an investment, at least not financially. It might be an investment in your happiness, your family, and your stability. All of that has value too, even if you can’t put a number on it.

I hope this article brought you some clarity if you’re debating between buying or renting. I want to add the calculator I used to mykronor so that you can play around with different numbers too. Subscribe below if you’d like to get notified when that happens.